Introduction

When most people start exploring insurance, two terms pop up again and again: insurance premium and sum assured. At first glance, they sound like complicated financial jargon. But once you understand them clearly, you’ll realize they are the backbone of any insurance policy.

In this blog, we’ll break down insurance premium vs sum assured in very simple words, show how they work in real life, and explain why knowing the difference can save you from big financial mistakes.

What is Insurance Premium?

Think of the premium as the price you pay to keep your insurance policy active.

- Just like you pay a monthly fee for Netflix or gym membership, in insurance you pay a premium.

- It can be paid monthly, quarterly, yearly, or sometimes as a single lump sum.

- Without paying the premium, your insurance coverage will lapse.

Example:

Mr. A buys a life insurance policy. The company tells him he must pay ₹12,000 per year to keep it valid. That ₹12,000 is the premium.

So in simple words: Premium = the cost of protection.

What is Sum Assured?

The sum assured is the amount the insurance company promises to pay your nominee or you (depending on the type of policy) if the insured event happens.

- In life insurance, it’s the money your family will receive if something happens to you.

- In health insurance, it’s the maximum medical expense the insurer will cover.

- In general insurancehttps://insuranceunfolded.com/general-insurance-coverage-explained/ (like motor or travel), it’s the maximum payout the insurer commits to.

Example:

Ms. B takes a health insurance policy with a sum assured of ₹5 lakh. If she gets hospitalized, the company will pay her medical bills up to ₹5 lakh.

So in short: Sum Assured = the guaranteed payout (coverage).

Insurance Premium vs Sum Assured: The Key Difference

| Factor | Insurance Premium | Sum Assured |

|---|---|---|

| Meaning | Amount you pay to keep the policy running | Maximum payout you or your family will get |

| Nature | Outgoing cost (your payment) | Incoming benefit (insurer’s payment) |

| Frequency | Paid regularly (monthly, yearly, lump sum) | Paid once, only when claim arises |

| Decided by | Age, health, lifestyle, type of policy, coverage | The amount you choose when buying the policy |

| Example | ₹12,000 yearly for life insurance | ₹10 lakh life cover |

The simple formula:

Premium = What you give.

Sum Assured = What you get.

Why Does Premium Depend on Sum Assured?

The higher the coverage (sum assured) you want, the higher the premium you’ll need to pay.

Example:

- Sum assured of ₹10 lakh → Premium ₹12,000 per year.

- Sum assured of ₹20 lakh → Premium ₹22,000 per year.

Why? Because the insurance company is taking on a bigger financial risk.

It’s just like buying a bigger house: more area = more cost.

Real-Life Example to Understand Better

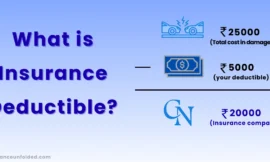

Imagine you are buying a car insurance policy.

- If your car is insured for ₹5 lakh (sum assured), and you meet with an accident causing total damage, the insurer will pay you up to ₹5 lakh.

- But to get this cover, you might be paying ₹10,000 annually as premium.

So premium is the “ticket price” you pay every year, and sum assured is the “benefit” you receive if something goes wrong.

Common Confusion: People Mix Them Up

Many people mistakenly think that premium = benefit. That’s not true.

Suppose you pay ₹15,000 premium every year for a life policy. That does not mean your family will get only ₹15,000. They will get the sum assured, say ₹25 lakh.

The premium is just your contribution to keep the coverage alive.

Factors That Decide Your Premium

Insurance companies calculate premium scientifically using something called underwriting. Key factors include:

- Age – Younger = lower premium.

- A 25-year-old may pay ₹8,000 per year for ₹10 lakh life cover.

- A 45-year-old may pay ₹20,000 for the same cover.

- Health Condition – Healthier = cheaper premium.

- Smokers, people with medical history, or lifestyle issues usually pay more.

- Type of Policy – Term insurance, endowment, health, or motor all have different premium structures.

- Sum Assured – Higher cover = higher premium.

Why Understanding the Difference Matters

Knowing insurance premium vs sum assured helps you:

- Choose wisely – Don’t go for the cheapest premium blindly; check if the sum assured is sufficient.

- Plan finances – Premium is your yearly expense; sum assured is your family’s future safety net.

- Avoid surprises – Many people realize later that they are underinsured (sum assured too low).

How to Decide the Right Sum Assured and Premium

- For Life Insurance

- A common rule: Sum assured should be at least 10–15 times your annual income.

- Example: If you earn ₹6 lakh/year, aim for ₹60–90 lakh sum assured.

- For Health Insurance

- Look at hospital costs in your city.

- Example: In metro cities, ₹5–10 lakh cover is now basic.

- For General Insurance (like car)

- Base it on the current value of your car or asset.

Balance is key: Choose a sum assured high enough for protection, but with a premium you can comfortably afford long-term.

Practical Example: Mr. X vs Mr. Y

- Mr. X buys life insurance with a sum assured of ₹50 lakh. Premium: ₹20,000/year.

- Mr. Y chooses only ₹10 lakh cover because the premium is cheaper: ₹6,000/year.

At first, Mr. Y feels he saved money. But if something happens, his family gets only ₹10 lakh, which is not enough to cover their expenses. Mr. X’s family, on the other hand, is financially secure with ₹50 lakh.

Lesson: Don’t judge policies only by low premium. Always check sum assured.

Conclusion

The debate of insurance premium vs sum assured is not about choosing one over the other. They are two sides of the same coin.

- Premium is the cost you pay to keep your protection alive.

- Sum Assured is the promise your insurer makes to secure your future.

Understanding this crucial difference will help you buy policies that actually serve their purpose—protecting you and your family when life throws challenges.

When you next sit with an insurance agent or browse policies online, ask yourself:

Am I focusing too much on premium, or am I choosing the right sum assured for real protection?

Because at the end of the day, the true value of insurance is not in what you pay, but in the security it brings.

{kind=link}

I am forever thought about this, regards for putting up.