Introduction

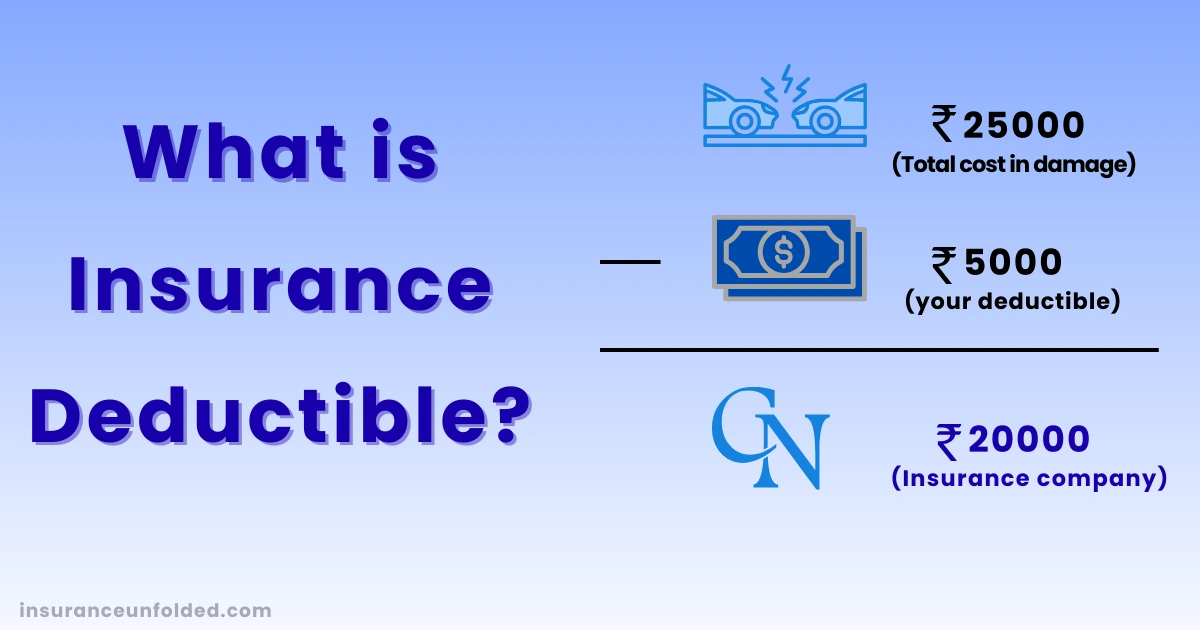

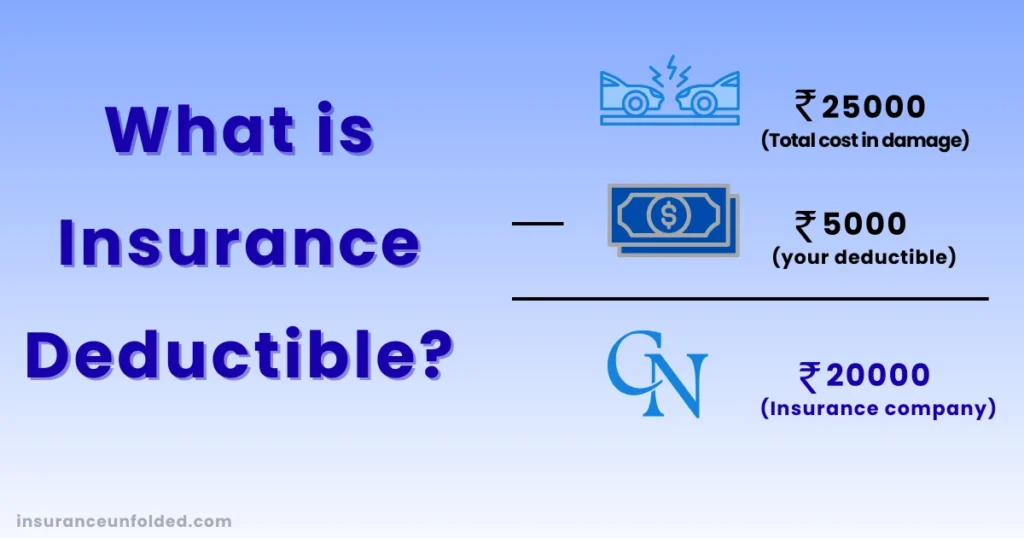

Insurance Deductible – This term is not as technical as it sounds. Deductible is the amount that you pay from your pocket at the time of claim, after which the insurance company pays the remaining amount.

Take a small example – if your health insurance has a deductible of ₹5,000 and the hospital bill comes to ₹30,000, then you will have to pay the first ₹5,000. After that the insurance company will pay the remaining amount of ₹25,000. Simple!

The problem arises when people buy insurance policies without understanding the concept of insurance deductible. As a result, they either pay a higher premium or are disappointed at the time of insurance claim. In this blog, we will understand the concept of insurance deductible in simple terms, how it works, its types, and most importantly, what is right for you

What is an insurance deductible?

As we understood above, deductible is a fixed amount which you have to pay from your pocket and after that the insurance company settles the remaining amount.

Insurance companies adopt this system to avoid every small claim. If the insurance company will pay every claim of ₹500-₹1000, then the insurance premium will become very high. Insurance deductible creates a balance between the insured and the insurer so that the insured understands his responsibility and the insurer also does his job properly without increasing the premium.

How does the insurance deductible work?

The process is simple :

- There is a loss or expense that the policy covers.

- You first pay the deductible amount.

- The insurance company pays the remaining money as a claim

For Example:

- Health insurance deductible = ₹5,000

- Hospital bill = ₹25,000

- You will pay ₹5,000 → Insurance will pay ₹20,000

Got it? Deductible is a kind of “first step” that you have to take before coverage starts.

Types of Insurance Deductibles

Different policies have different types of deductibles. There are four common types:

1. Flat deductible

This is a fixed amount payable on each claim. For example, Rs 10,000 on a car insurance claim.

2. Percentage deductible

This deductible is a percentage of the sum insured. For example, 2% of the insured value in property insurance.

3. Annual deductible

Fixed amount of money you pay out-of-pocket for medical expenses before your health insurance company starts covering the costs. The deductible amount is usually reset every year, so you need to meet it again in the following policy year.

4. Per-claim deductible

A different deductible applies to each claim. If you make 3 claims, you will have to pay the deductible 3 times.

Real-life Examples of deductibles

- Health Insurance: Deductible ₹10,000. If the bill is for ₹80,000 then you will pay ₹10,000, and the insurer will pay ₹70,000.

- Car Insurance: Deductible ₹7,500. The repair cost is ₹50,000. You will pay ₹7,500, and the insurance will pay ₹42,500.

- Travel Insurance: Deductible ₹2,000. If the luggage loss claim is for ₹20,000, the insurance will pay ₹18,000.

See? This is just your contribution, not extra money.

Insurance Deductible vs Premium

Some people also get confused between insurance deductible and insurance premium, while both are completely different:

- Premium: The money you pay every month/year to keep the policy active.

- Deductible: The money you pay from your pocket at the time of claim.

And the relation between these two is simple :

- Higher deductible → Lower premium

- Lower deductible → Higher premium

Simple formula: If you take more responsibility, then the insurance company takes less premium from you.

Higher vs Lower Deductible : What to choose?

This is a common question – is it better to take high deductible or low?

- Higher Deductible

- Premium is less

- If claims are less then money is saved

You will have to keep more cash ready at the time of claim.

- Lower diductible

- Less expense at time of claim

- More peace of mind

Premium will be higher.

So the choice depends on your financial comfort.

How to Choose the Right Deductible?

The right deductible can be chosen by using a little calculation and common sense:

- Look at the budget: If you can easily pay ₹10,000–₹20,000 in one go, then save the premium by taking a higher deductible.

- Check your lifestyle: Frequent doctor visits? Daily heavy driving? Then a lower deductible is better.

- Keep a balance: Neither a very high deductible that seems risky, nor a very low one that will inflate the premium.

Common Myths About Deductibles

Deductible is an extra charge

No. This is just the first part of the claim that you cover. In a way, it is your contribution.

High deductible is always the best.

Not true. You will always have to keep that much cash ready and there can be a problem in case of emergency

Health insurance has a deductible on every claim

Not necessary. Many plans keep an annual deductible which is paid only once a year

Conclusion

So now in summary: Insurance deductible simply means that you will pay the first part of the claim (equal to the deductible), the rest will be handled by the insurer.

- This system makes it affordable by reducing the premiums

- Filters out small and big claims

- And also makes policyholders responsible

The right deductible for you will be the one that balances your budget and risk level. Choose a high deductible only when you have savings for emergencies. If you want to remain tension-free, take a low deductible, even if the premium is a little high.

Finally remember one thing: Understanding the deductible is a big step in understanding insurance. If this is clear, then choosing the policy and making a claim both become easy.

{kind=link}

Pingback: Step-by-step Guide to Easily Calculate Insurance Coverage - Insurance Unfolded

Pingback: 5 Common Insurance Mistakes to avoid - Insurance Unfolded

Pingback: How to Choose the Best Health Insurance With Maternity Benefits - Insurance Unfolded